Buzzwords such as ‘Artificial Intelligence’, ‘Machine Learning’, ‘Chatbots’ and ‘Robo-Advisors’ are rather ubiquitous among bankers and non-bankers alike. They are prominently echoed in boardrooms and earnings calls of large corporations, and increasingly feature in their quarterly reports. A few years ago, these ideas were merely discussed and not much was done to act on any of them. This could either be because of the lack of knowledge regarding the potential benefits these new technologies brought in, or because of the supposedly more important ‘strategic’ initiatives piled up on the desks of top management. This attitude has significantly changed over the past few years – one can notice a tectonic shift in the adoption of disruptive technologies for streamlining business processes, and in turn reducing costs and increasing efficiency. Large enterprises are implementing sophisticated solutions to internal processes, as well as to customer facing services, by using automation to replace repetitive, human tasks.

One such improvement in recent years has come in the form of Chatbots. The word ‘chatbot’ is a beautiful amalgamation of two of mankind’s most recent obsessions: messaging (chat) and robots (bots). Until recently, chatbots featured more in science fiction than in the real world. Few were able to fathom the explosive growth that was to occur. With the introduction of Siri, Alexa, and Google Assistant a few years ago, this bit of science fiction became a reality.

Chatbots are software programs that use real-time messaging as an interface. With extensive, and precise mapping of (potential) conversations, chatbots pose a serious threat to the age-old concept of a contact center. We now live in an instant gratification society, where waiting for an attendant at the opposite end has become a hindrance. In a world inhabited by digital natives, EVERYTHING IS INSTANT; from Instant Coffee & Noodles, to the more recent, Instant Customer Service. Chatbots are trying to address the latter, by providing real-time responses to customer queries. Be it rule-based or AI-driven, chatbots are slowly becoming the preferred form of communication for customers of all ages.

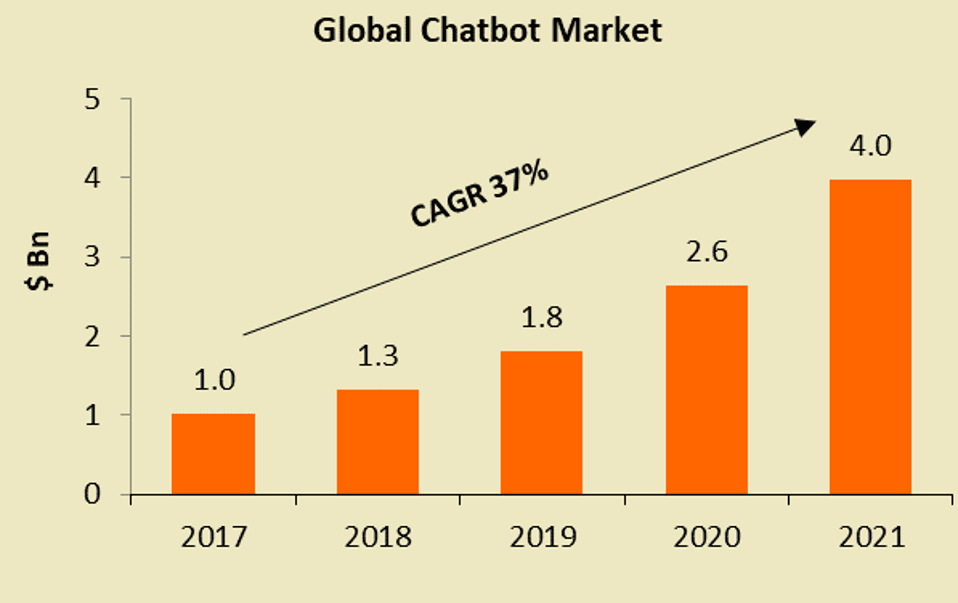

As a market valued at a little over $1 Bn in 2017 and predicted to reach $4 Bn by 2021, chatbots are set to grow at a CAGR of 37% over the coming 4-5 years. Looking at India for instance, in 2017, there were over 150 million users of messaging apps. This number is expected to grow at a CAGR of 17% over the next 3-4 years to 231 million users. With such rapid growth expected, companies are poised to ride the ‘chatbot’ bandwagon. This growth is driven by an increasing number of users relying on messaging apps, such as Facebook Messenger, Slack, and Telegram. In terms of cost reduction, chatbots will be responsible for annual savings of ~$8 Bn by 2022. And in terms of increased efficiency, a chatbot inquiry will save more than 4 minutes per call in comparison to traditional call centers. Is it surprising then, that enterprises are increasingly moving towards chatbots to reduce costs?

For any company, cost reduction and increased efficiency are in fact, imperative to its bottom line. What a chatbot, an automated chat interface, brings to the table is the ability to replace archaic contact centers, with a modern, instant service platform, at a fraction of the cost. A testament to the growth of messaging apps, and in turn to the rise of chatbots, is in its popularity; the top messaging apps garner a larger daily/monthly audience than the top social networks.

Source: Business Insider, IBS Intelligence

Source: Business Insider, IBS Intelligence

Translating this growth into tangible results for the financial services industry, is what many institutions are trying to unravel. Selling financial concepts is difficult, not because of the competition, but because of the prevalent status quo of doing nothing. There is a ton of information available, but this information is not designed to be digested by millennials, as well as by senior citizens. This is where Chatbots jump in! They can be positioned as utility tools to promote ‘Financial Literacy’, and disseminate information based on customers’ needs. For e.g., a Brokerage house can use chatbots to ‘educate’ new/existing users about the convoluted world of equity markets. Using an automated chat interface, complex financial terms and concepts can be simply explained, even to a novice. Typically, a chatbot determines the suitability of a product for a customer by assessing the financial health of his/her portfolio, along with the respective goals. The chatbot then recommends what products the customer should invest in, and what proportion of his/her wealth should be invested in different product types. The core objective is to empower the end user, who can then make informed monetary decisions after thorough assessment of the relevant products. The idea is to systematically break down complex financial content into conversational snippets within a chat interface. The content should be designed to enable the user to understand concepts and financial processes with ease, so as to bridge the gap in his/her understanding.

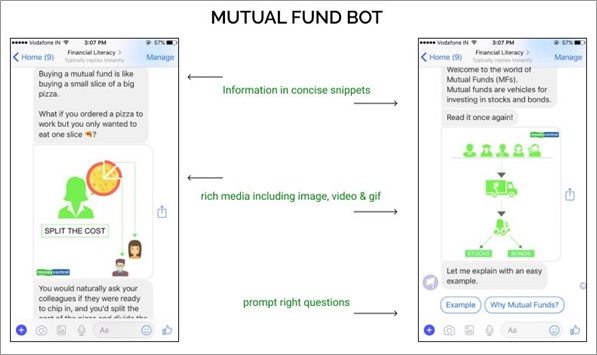

Source: Mpower.chatLet’s take Mutual Funds as an example. In India, Mutual Funds are becoming commonplace, given that they strike the right balance of being highly profitable, yet relatively safe. The share of MFs in the overall asset pie is increasing. There are numerous first-time investors looking to channel their moderate savings into high yield investments.

Source: Mpower.chatLet’s take Mutual Funds as an example. In India, Mutual Funds are becoming commonplace, given that they strike the right balance of being highly profitable, yet relatively safe. The share of MFs in the overall asset pie is increasing. There are numerous first-time investors looking to channel their moderate savings into high yield investments.

Although, the process of investing in Mutual Funds may seem straightforward, it is riddled with roadblocks (e.g., lack of financial know-how), some of which can easily (and rapidly) be countered with the help of chatbots. An effective chatbot can resolve certain customer queries within seconds, and if executed accurately, can put the customer at ease, thereby increasing his/her propensity to move ahead with that particular product or service.

On the banking side of things, large financial institutions such as Citi, Bank of America and Capital One have implemented their versions of chatbots, which customers can access through the respective mobile apps, Facebook Messenger, Twitter or regular text messages (SMS). At Citi and Capital One for example, customers can check their account balances, recent transactions, payment history, credit card bill summary, and avail many other non-financial services. Answering FAQs is one of the other key service areas where banks have excelled. All of these services collectively provide the user with real-time, easily accessible customer information. As a natural move forward, albeit on the slower side, banks are now implementing chatbots that allow customers to carry out financial transactions on their platforms; something that seemed generations away, doesn’t seem that far-fetched after all.

The need of the hour is communication, with its delivery through messaging applications dominating the social media & messaging landscape. These applications have far surpassed social media in terms of total users as well as total time spent. There are over 300 million people across India alone that have access to the Internet on their smartphones today, and India is embracing the Internet in a way we could not have imagined before. Keeping this development in mind, imagine a world where we use automated chatbots to not only breakdown financial concepts for seasoned smartphone users, but also help new internet users navigate through a plethora of financial information. The idea is to spread financial literacy, and create a more meaningful customer journey, from curiosity to execution. And chatbots make this accessible, by reaching customers via apps they already use – WhatsApp, Facebook Messenger, and Twitter – rather than making clients download additional apps.

The advent of chatbots (messengers, as well as voice recognition applications) has allowed companies to penetrate, through smartphones, the potential user base like never before. The primary use case for chatbots, in this day and age, is non-financial in nature. Most financial institutions allow customers to access only basic product information, and information regarding certain processes on their chatbots. However, with regulatory authorities taking a closer look at integrating such technologies into financial transactions, it won’t be too long until we can safely say “Alexa, please transfer $500 to Patrick this Thursday”, and rest easy.

By Abhijit Aroskar,

Consultant,

Cedar Management Consulting.