September 23, 2025

Imagine this: A bank sets out to test an AI-driven credit scoring model. In the traditional setup, the process drags on for months, involving building infrastructure, navigating approvals, sourcing data, and setting up test environments. By the time a Proof of Concept (POC) is ready, the market opportunity may already have slipped away.

A virtual sandbox changes that equation. It enables the same POC to be designed, tested, and validated in weeks instead of months. That’s speed with survival built in an edge no bank can afford to ignore in today’s FinTech race.

Why Sandboxes Matter in Banking Today

Banks are under constant pressure to innovate. Customer expectations are shaped by the Amazons and Ubers of the world: instant, seamless, hyper-personalized. Regulators are pushing for stronger compliance while investors demand efficiency. That means banks need safe, fast, and scalable spaces to experiment without risk.

This is where sandbox environments, virtual, cloud-based, secure replicas of real systems, become game-changers. They let banks simulate real-world scenarios using synthetic or anonymized data, while isolating innovation from core systems.

According to the World Bank, over 70 jurisdictions globally have introduced regulatory sandboxes since 2016. The UK’s Financial Conduct Authority (FCA) sandbox alone has hosted over 150 FinTechs, with 90% going on to commercial launch. In India, RBI’s regulatory sandbox cohorts have fast-tracked innovations in cross-border payments, offline UPI, and retail lending.

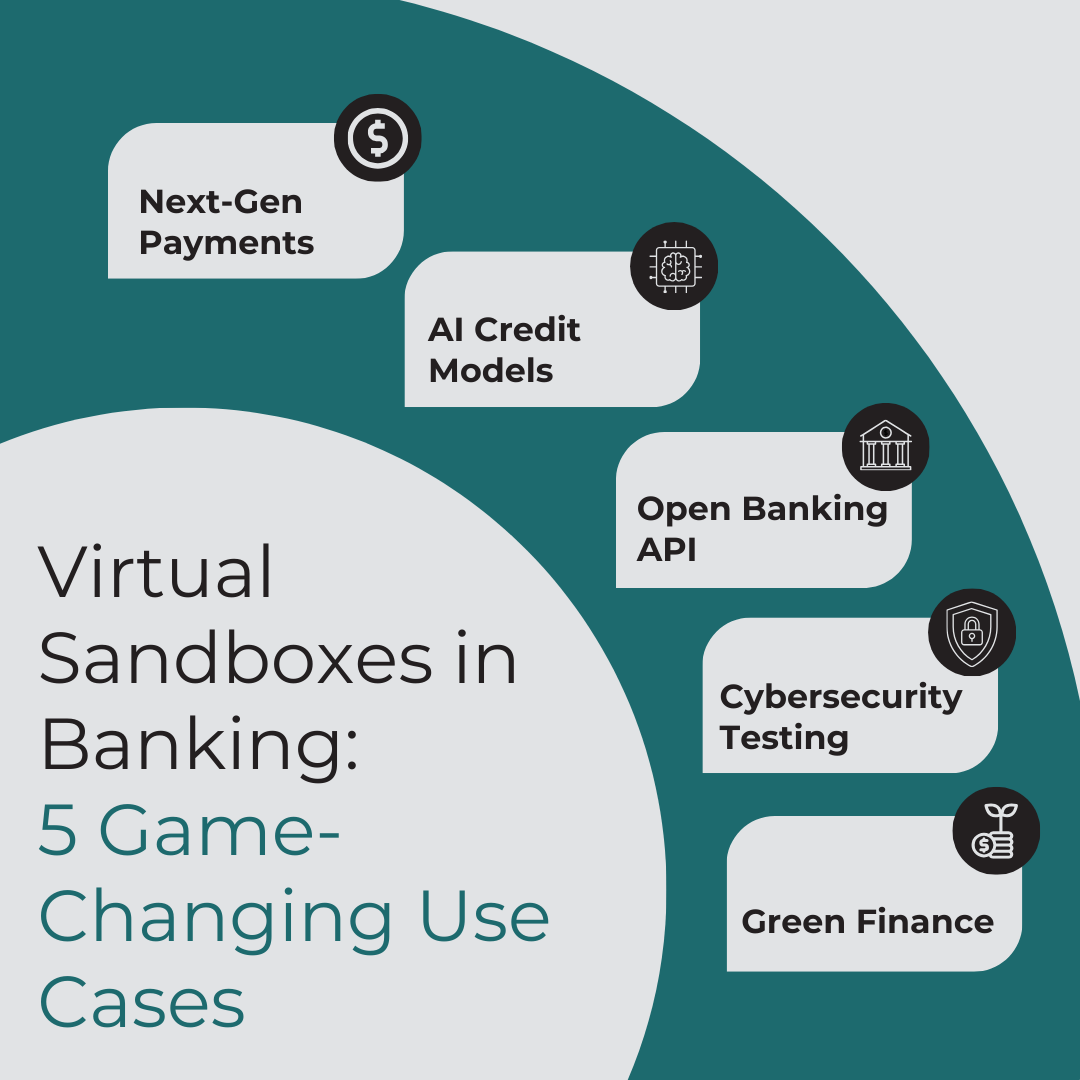

Use Cases: Transforming POCs in Banking

- Next-Gen Payments (UPI, CBDCs, Cross-border Rails)

- Banks can trial new payment methods; whether it’s a CBDC pilot or a UPI-like instant payments layer for another market, without disrupting live customer flows.

- Example: The RBI’s CBDC sandbox pilots in 2023 enabled multiple banks to test wholesale and retail digital rupee transactions in isolated environments before live rollouts.

- AI-Driven Credit Models

- Sandboxes allow secure testing of AI/ML models for underwriting, fraud detection, and risk scoring on synthetic data.

- Banks using AI-based credit models reduce loan processing time by up to 70%. Testing them in sandboxes accelerates deployment while meeting data privacy norms.

- Open Banking & API Integrations

- In an era of Banking-as-a-Service (BaaS), sandboxes are critical for testing third-party APIs.

- India’s Account Aggregator framework, which connects consent-based financial data across banks, relies on sandbox setups to onboard new FinTechs quickly and safely.

- Cybersecurity Stress Testing

- Banks can simulate cyber-attacks or fraud attempts on virtual replicas without risking real systems.

- The European Banking Authority (EBA) recently encouraged sandbox-style red-team testing to meet growing cyber resilience mandates.

- Sustainability & Green Finance Products

- New ESG-linked loan structures or carbon-credit marketplaces can be trialled in sandboxes before market launch.

- Example: Singapore’s MAS has been funding green FinTech pilots using sandbox frameworks, supporting banks in testing blockchain-based carbon trading platforms.

The Impact: Faster POCs, Lower Costs, Better Innovation

- Speed: Virtual sandboxes can cut POC cycles from 6–12 months to as little as 6–8 weeks.

- Cost Efficiency: No need for heavy upfront infrastructure; cloud-based sandboxes scale on demand.

- Compliance Ready: Built-in guardrails ensure that even experimental projects adhere to regulatory norms.

- Collaboration Friendly: Banks, FinTechs, and regulators can co-create within the same environment, reducing silos.

A report in 2024 revealed that banks using sandbox-driven POCs achieved 40% faster time-to-market for digital products compared to those using traditional development setups.

Looking Ahead: Virtual Sandboxes as a Strategic Weapon

As banking becomes more digital and interconnected, sandbox adoption will move from optional to essential. In fact, it is predicted that by 2027, 60% of Tier-1 banks will have dedicated sandbox platforms to validate at least half their digital initiatives.

The next frontier? Global interconnected sandboxes. Imagine a future where banks in India, Singapore, and the UAE can test cross-border payment rails in a joint sandbox, accelerating regulatory alignment and product launches at a global scale.

What This Means for You

If you’re a banker, FinTech founder, or investor, sandboxes aren’t just a tech tool; they’re a strategic lever. They shorten innovation cycles, reduce risks, and foster collaboration.

At Cedar-IBSi FinTech Lab, we see virtual sandboxes not as experimental toys, but as launchpads for real transformation. From credit innovation to CBDCs, the ability to test quickly, fail safely, and scale rapidly will determine who leads the future of banking.

The question is: will you just watch the sandbox revolution, or build your next big idea inside one?