As corporate banks look towards a post-Covid era, what Innovations should transaction banking heads fast track in 2021?

By Chetan Parekh, Partner Cedar Management Consulting International LLC

Covid-19 slowed down corporate and institutional business and, together with lower interest rates, has created a margin squeeze for corporate banks. Corporate income pools are shifting in a big way from interest to fees-based income from global transaction banking (GTB) services. GTB platforms have not only become important from the fee income perspective but they also enable corporate banks to lower costs due to innovation and STP enablement. GTB cash management services like liquidity management, collections, receivables, and payments are expected to contribute 60-70% of global transaction banking market revenues followed by trade finance and supply chain. This is a $1 trillion opportunity globally and worth $8 billion in the Middle East, according to recent research.

GTB business services are going through disruption with FinTechs, which are playing a pivotal role, providing both complementary and competitive offerings to corporate banks. Areas such as trade finance and supply chain finance are moving from paper-based documentary credit business to blockchain-based smart contracts. Even banks’ supply chain finance businesses are moving from simple factoring products and supplier financing products to innovative buyer-led programmes, reducing the cost of risk for global corporate banks.

Why innovate?

It is imperative that banks look to digitising their corporate banking transaction volumes in order to remain competitive and improve accuracy and speed of transaction. The digital revolution is affecting the business at large and the choice is simple: either to be the disruptor or the disrupted! Innovation in services for a disruptor can offer an edge. Hence, many corporate banks are structurally moving income pools from interest to fees-based services through FinTech innovations. Note that JP Morgan invests $11 billion annually in ‘Future Tech’ to drive innovation.

How to innovate?

There are two major ways for corporate banks to transform their platforms: building a digital platform of choice using ‘agile’ practices greenfield; or, second, “buy/partner” with GTB platform and FinTech solutions. Each model comes with its pros and cons, and suitability based on size of bank, its clients, and its capabilities. For example, French bank BNP Paribas transformed and innovated its GTB platform with the latter approach, with an eco-system of FinTech players and a platform of repute from global solutions provider Finastra.

Innovation requires a bank to identify segments and key unmet needs or pain points and then apply a design thinking-based approach to identify and build solutions. FinTechs can be very handy to reduce time to build and provide sustainable solutions over the cloud. Most FinTech programmes have only 90-180 days launch time, offering quick-tomarket solutions for large corporates and SMEs.

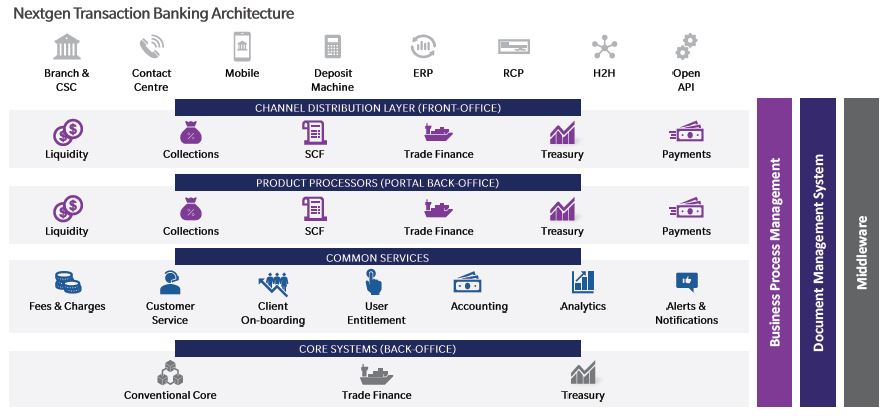

Banks must start to innovate by building an architectural blueprint, which is flexible at multiple layers from front, middle and back offices, including common services and de-coupling, and leveraging their back office platforms like core banking, treasury, and trade finance. The plan should allow corporate banks to have multiple vendor solutions that can co-exist from build to buy and partnering with FinTechs through API based integrations through Open API.

Innovation 1 | Open B2B APIs

Many banks over the years have built monolithic transaction banking systems and proprietary Host-2-Host adapters with their corporate customers. These are now giving way to API-based B2B services. This is not only faster but much more economical. In a recent survey of banking executives, more than 60% of them are investing in B2B API solutions.

There is a clear business case for the B2B APIs in the areas of cash management, payments, invoice reconciliation, and working capital financing. The platforms being rolled out globally by regulators and, for example, unified payment systems in India are enabling banks to further leverage API platforms. Once moved onto a B2B API platform, a bank may consider how expensive and cumbersome H2H proprietary platforms may be retired in a phased manner.

Innovation 2 | Build smart onboarding by segment

Corporate banks have traditionally followed an RM and branch/ service centre-based opening of relationship. The time has come to innovate across segments and build a digital onboarding solution. Banks should look to develop a solution for self-service onboarding for small and medium size corporates in partnership with local chambers of commerce and registrars of companies along with start-of-the-art authentication solutions. Consider innovations such as “Click and Sign” (as already approved by the European Union). You may also bundle a small to medium size ERP solution.

Develop assisted onboarding for medium and large corporate and institutional clients, allowing RMs to have tablet-based apps with information services such as Moody’s being integrated for credit appraisal information. The objective here should be to make your RM invest most time in relationship building and offering customised solutions, and let his tablet CRM do the onboarding!

Innovation 3 | Drive your digital SME bank

The SME sector is an important business segment for corporate banks with 80-85% of clients falling within this segment for commercial banks. Financial institutions should strongly consider offering a digital SME banking solution, whereby onboarding, account services, salary processing, payments and certain basic trade services are offered through a digital platform well supported by virtual RMs and BOTs.

Innovation 4 | Digitise through blockchain and smart contracts

The trade finance business is being disrupted. Blockchain and distributed ledgers are here to stay. Documentation secured delivery and contracting were material pain points in the industry which are resolved through a consortium-based approach. Invest carefully, adoption needs to be measured to avoid the pitfall of investing in technology without measurable returns. Know your clients, understand the market realities and counter party readiness to transact. For example, in Citi’s CitiDirect BE trade services portal import L/C are assigned by a counter party digitally and processes automated, reducing both operational cost and the risks involved in physical documentation.

Innovation 5 | Partner with Cloud based SCF Platform with Ecosystem

Up to 10% of the revenue pool of corporate banks will be based on supply chain finance (SCF) products such as factoring, supplier finance, receivables finance and buyer-led programmes. These niche lines of businesses are very interesting and help banks in distributing risk across the SME customer portfolio. Many of these products may be offered via a platform with limited RM or operational interaction. Partnering with an SCF platform, within an ecosystem could be very rewarding for corporate banks as it brings in digitally originated and highly scalable business. Products such as distributor financing and buyer financing are low risk, high income products. There are multiple platforms available from suppliers such as Codix, HPD Lendscape, Neurosoft, Premium Technology, Aranova and Demica to name a select few. Banks also have the option to put this solution on cloud or on premise.

In summary, corporate banks must innovate, developing GTB platforms either by build or buy/partner with FinTech. They should create a flexible GTB system architecture, which allows the bank to invest into FinTech opportunities to build differentiated products and services for its business segments. Investment in next generation technology architecture offers the potential to disrupt the market, acquire clients at rapid pace and lead the way for industry rather than being disrupted!