The Critical Role of Fraud Management in Scaling B2B FinTech Startups

October 16, 2024

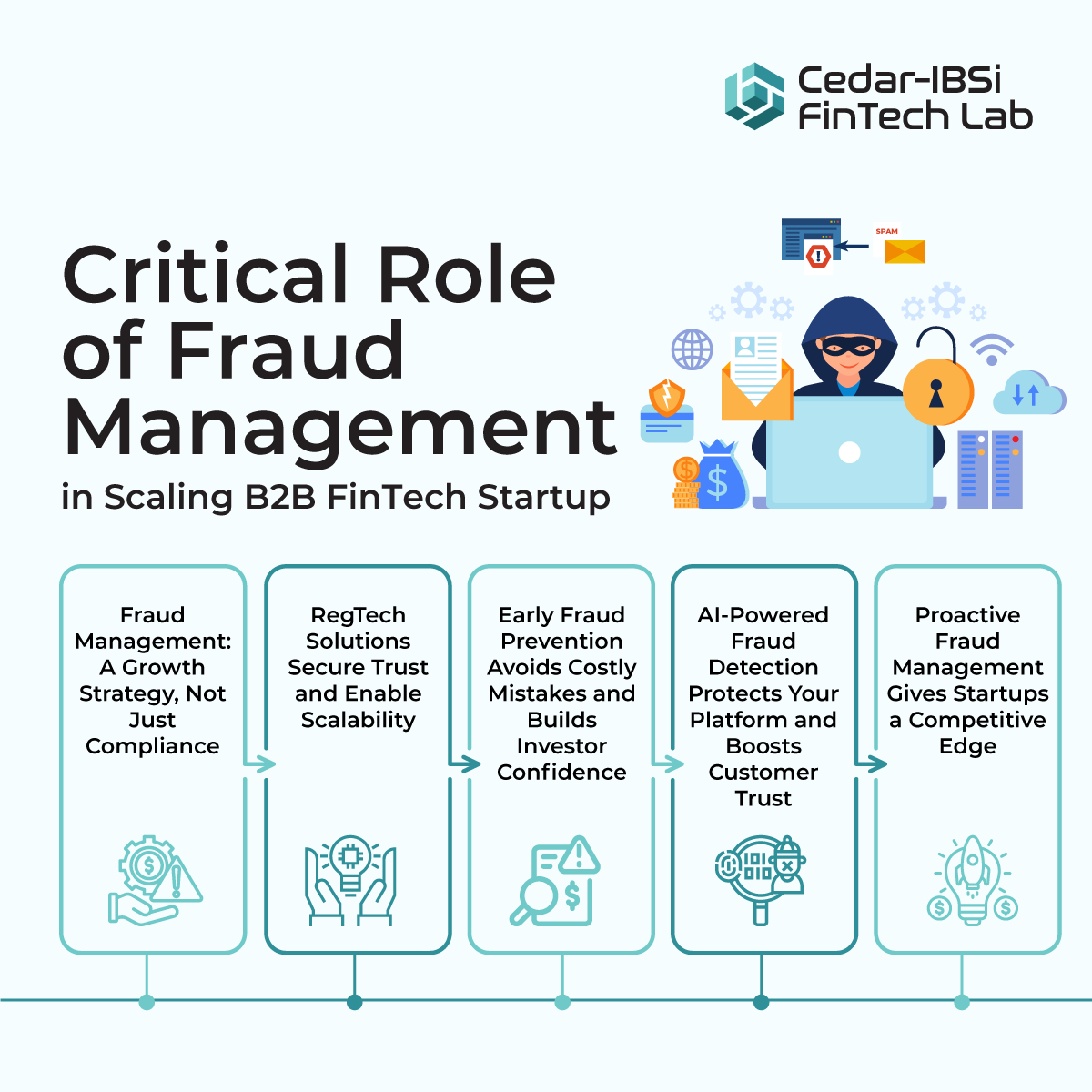

In the fast-paced world of B2B FinTech, fraud management is not just a regulatory checkbox—it’s a cornerstone of sustainable growth and long-term success. Managing fraud is not just about compliance; you have to protect your business, customers, and reputation. For FinTech founders, especially those aiming to scale, addressing fraud early can save you from costly mistakes down the line. This blog underscores the paramount importance of integrating RegTech based fraud management solutions into B2B FinTech operations right from the outset.

As the volume of sensitive financial data and transactions handled by FinTechs increase, fraudsters too become more sophisticated. Without solid fraud prevention measures in place, a single breach can lead to significant financial losses, reputational damage, and loss of customer trust. These factors can be devastating for a young company. In the B2B space, where partnerships and trust are paramount, companies that fail to prevent fraud early on may struggle to secure long-term relationships or attract further investment.

Fraud management is a competitive advantage. Prioritizing robust fraud prevention strategies signals to your customers and investors that you take risk management seriously. This can set you apart in a crowded market.

B2B FinTech is also highly sensitive to disruptions. If your platform is seen as vulnerable to fraud, larger corporate clients will hesitate to trust you with their transactions. This is especially critical when dealing with financial institutions, enterprise-level clients, or international payments. By embedding fraud prevention into your core systems from day one, you are essentially future proofing your operations and showing clients and investors that you have a plan for scalability.

Enter RegTech; transforming how FinTech companies handle fraud detection and compliance. By using advanced technologies like AI and machine learning, RegTech can monitor real-time transactions, flag suspicious activities, and ensure ongoing compliance with global regulations. These automated tools reduce the complexity of regulatory frameworks, freeing up your team to focus on growth while also protecting your platform from bad actors.

Integrating RegTech solutions early equips you better to handle fraud and makes you more appealing to investors. Venture Capital (VC) companies are increasingly looking for startups that have these systems in place, as they reduce operational risk and demonstrate a clear path to scaling without regulatory hiccups. These startups also enjoy the perception of a low-risk investment with high potential returns, as a result of regulatory readiness and operational integrity.

Take, for example, B2B payment platforms that integrated RegTech-driven fraud management systems from the start. These startups not only managed to avoid costly breaches but also earned trust from enterprise clients, enabling faster onboarding and expansion. By focusing on fraud management from the beginning, they positioned themselves as reliable partners, which attracted additional funding and strategic partnerships.

Secure Pay Solutions, a startup offering B2B lending services that has prioritized fraud management, earned the trust of both clients and VCs. Their well-structured fraud prevention strategy became a key differentiator, helping them stand out in a crowded market and attract significant investment.

For B2B FinTech startups, integrating fraud management solutions from day one is first, a strategic imperative, and then a regulatory mandate. A robust fraud prevention framework can protect customer data, build investor confidence, and drive growth. Startups that recognize and act on this insight are better prepared to thrive in the competitive FinTech landscape and build themselves a secure and scalable future.

How Cloud-Native Infrastructure is Reshaping Core Banking System

September 26, 2024

In the digital age, banking has rapidly evolved, with customers demanding seamless, 24/7 services. Many banks remain burdened by legacy core banking systems that limit their ability to meet these demands. These older systems often struggle to integrate modern technologies such as artificial intelligence (AI), machine learning (ML), and real-time analytics, resulting in increased operational costs and reduced agility.

In this rapidly evolving landscape of financial services, core banking systems need significant transformation. The advent of cloud-native infrastructure is at the forefront of this revolution, offering unprecedented agility, scalability and efficiency.

What is Cloud-Native Infrastructure?

Cloud-native infrastructure is a set of technologies and practices that enable the development and deployment of applications in the cloud. It is characterized by microservices, containers, and continuous delivery pipelines.

Microservices: Microservices are small, independent services that work together to form a larger application. This modular approach makes it easier to develop, test, and deploy applications.

Containers: Containers are lightweight, portable units of software that package up an application and its dependencies. This makes it easier to move applications between different environments.

Continuous delivery pipelines: Continuous delivery pipelines automate the process of building, testing and deploying applications. This helps to ensure that applications are always up-to-date and reliable.

How Cloud-Native Infrastructure is Reshaping Core Banking Systems

Moving core banking systems to a cloud-native architecture offers numerous advantages.

Enhanced Security: Security is a top priority for any financial institution. Cloud-native infrastructure offers advanced security features, such as automated patch management, encryption and continuous monitoring. These capabilities help banks protect sensitive data and comply with stringent regulatory requirements.

Faster Time-to-Market: In the competitive banking sector, the ability to quickly launch new products and services is a significant advantage. Cloud-native systems enable rapid development and deployment cycles, allowing banks to respond swiftly to market changes and customer needs. This agility fosters innovation and helps banks stay ahead of the competition.

Scalability and Flexibility: Cloud-native infrastructure allows banks to scale their operations effortlessly. Whether it’s handling a surge in transactions during peak times or expanding services to new regions, cloud-native systems can dynamically adjust to meet demand. This flexibility is crucial for banks looking to innovate and grow without being hampered by their IT infrastructure.

Real-World Applications

Emirates NBD, one of the largest banking groups in the Middle East, has been at the forefront of adopting cloud-native technologies. The bank has implemented a cloud-native core banking system to enhance its digital banking services. This transition has enabled Emirates NBD to offer more personalized and responsive services, improve operational efficiency and rapidly deploy new features to meet customer demands.

Mashreq Bank, another major player in the GCC region, has leveraged cloud-native infrastructure to drive its digital transformation. By adopting microservices architecture and containerization, the bank has been able to scale its operations dynamically and enhance its customer experience. The bank’s cloud-native approach has also facilitated the integration of advanced analytics and artificial intelligence, enabling more informed decision-making and innovative product offerings.

Capital One is another notable example. The bank has been a pioneer in adopting cloud-native infrastructure, migrating its entire data centre operations to the cloud. This move has not only reduced operational costs but also enhanced the bank’s ability to innovate. Capital One now uses cloud-native technologies to leverage big data and machine learning, providing customers with tailored financial advice and fraud detection services.

State Bank of India (SBI), the largest public sector bank in India, has adopted cloud-native technologies to support its digital transformation initiatives. SBI’s cloud-native infrastructure has enabled the bank to handle large volumes of transactions efficiently, enhance its cybersecurity measures, and offer a seamless banking experience to its customers. The bank’s cloud-native approach has also facilitated the integration of new technologies such as blockchain and artificial intelligence.

Cloud-native infrastructure is not just a technological trend; it’s a strategic imperative for banks. By embracing cloud-native technologies, banks can position themselves for long-term success in a rapidly evolving digital landscape. As the banking industry continues to innovate, cloud-native infrastructure will play a pivotal role in shaping the future of core banking systems.