Driving Financial Services on ONDC: An Invitation to Tech Innovators and Banks

August 26, 2024

The digital commerce landscape is undergoing a transformative shift with the advent of the Open Network for Digital Commerce (ONDC). This initiative is not just a platform but a movement towards a more inclusive and competitive marketplace. For banks and technology companies, ONDC represents a frontier of opportunities to redefine financial services. Central to this transformation are technology providers (TSPs), whose contributions are crucial in expanding ONDC’s reach.

Why ONDC Matters

ONDC’s purpose is to democratise the access to suppliers and create a platform for buyers across various industries. ONDC’s decentralised, node-based architecture allows for greater market access and competition. This approach ensures that smaller merchants can participate on equal footing with larger enterprises, thereby democratising digital commerce. ONDC does not operate as a traditional marketplace with a centralised front-end or back-end. Instead, it functions as a decentralised network where various participants, including buyers, sellers, and technology service providers (TSPs), can interact and transact seamlessly. The platform emphasises high-provenance data flow and connectivity, ensuring that all transactions are secure and transparent.

The ONDC Advantage

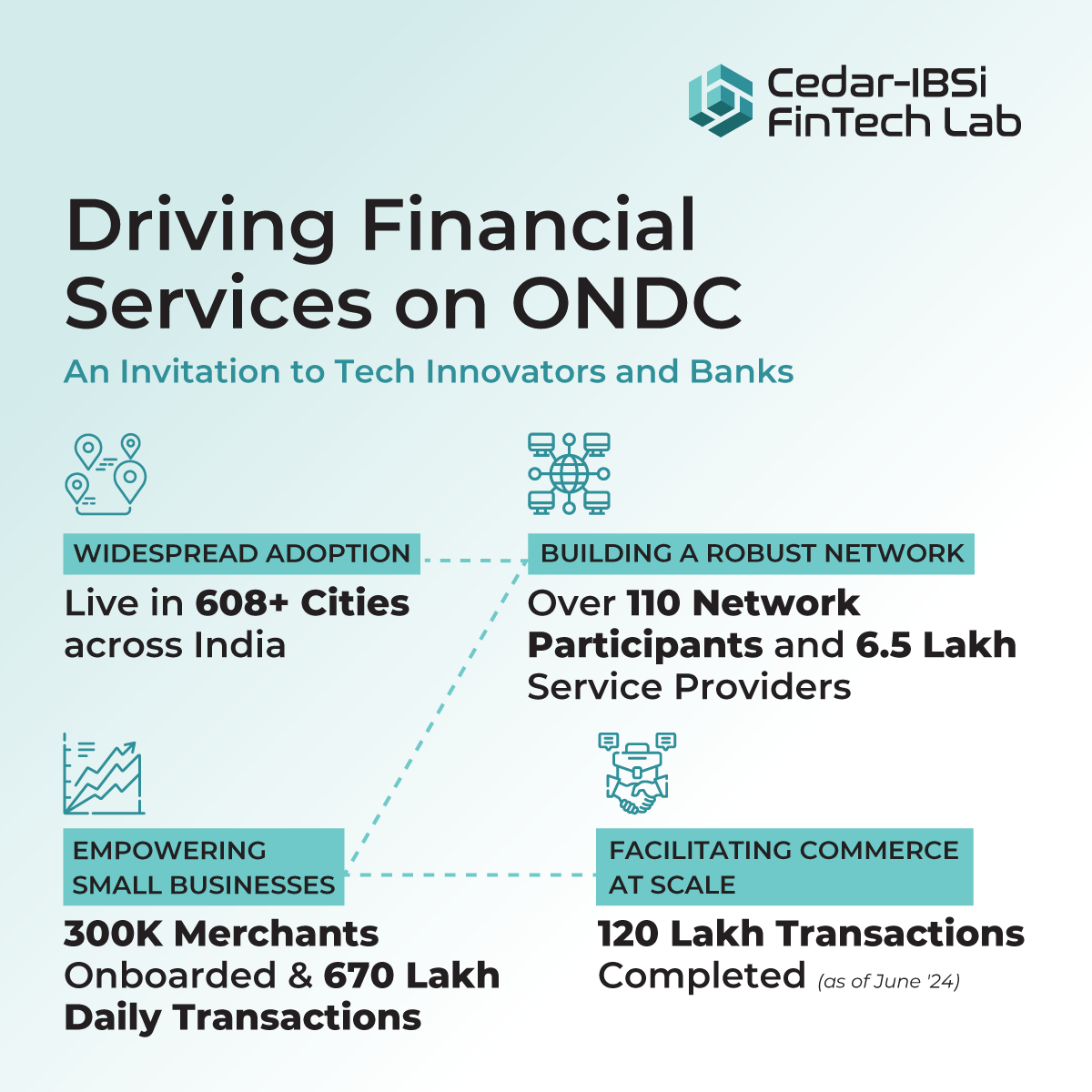

The platform works differently from traditional online shopping sites. It doesn’t have a usual front-end or back-end. Instead, it acts as a marketplace where different users can connect and do business, making data flow more secure and benefiting everyone involved. As of July 2024, the platform is live in 608+ cities with 10 domains including the financial services domain of access to credit. The platform has 110 network participants with 6.5 Lakh sellers/service providers. The platform has fulfilled 120 Lakh cumulative transactions till June 2024.

Expanding Financial Service Distribution

For banks and FinTech firms, ONDC offers a groundbreaking opportunity to reach new markets by building a strong distribution layer that connects seamlessly with various sell-side apps.

Thanks to ONDC’s node-based architecture, technology providers can facilitate these connections, allowing financial institutions to tap into a broader customer base, including those in rural and remote areas. The platform’s low-cost participation model, supported by TSPs, makes it easier for financial services to integrate and scale within the ONDC ecosystem, thereby lowering barriers to entry.

For instance, an NBFC based in a metro city like Mumbai will not plan to open a physical branch in rural region due to the high cost of operations and customer service. However, through the ONDC framework, they can lend to a consumer in the rural most region of the country expanding their distribution reach seamlessly. This is a critical aspect of financial inclusion, as it allows financial services to be more accessible and relevant to different segments of society.

Advancing Product Sachetisation and Financial Inclusion

One of ONDC’s key strategies is product sachetisation—offering small, easy-to-access financial products like micro-loans, small-ticket mutual funds, and term insurance. Technology providers play a vital role in this by creating the digital infrastructure that makes these products available on the platform. By supporting the distribution of these small-scale financial products, TSPs help financial institutions reach a broader audience, especially those who have historically been excluded from traditional banking services.

This strategy aligns perfectly with ONDC’s mission of promoting financial inclusion. This democratisation of financial services is a significant step toward bridging the financial inclusion gap in India.

Role of Technology Service Providers

Technology Service Providers (TSPs) are crucial in offering a range of software applications either as standalone solutions or via cloud-based services. TSPs enable seamless business operations on the network, empowering players to participate in e-commerce without requiring in-house technology capabilities. TSPs also serve as drivers for achieving ONDC goals and attracting businesses of various sizes to join the network.

Conclusion

As ONDC continues to grow, with around 300,000 merchants onboarded and 6.7 million daily transactions, the potential for financial services integration is immense. Early adopters like DMI Finance and Aditya Birla Finance have already connected with the ONDC network, and several other financial institutions are in the process of joining.

Banks and FinTechs must align with ONDC’s objectives to provide credit for income generation, insurance for protection, and mutual funds for wealth accumulation. Technology providers play a crucial and dynamic role in the success of ONDC, particularly in the realm of financial services.

It is imperative that the technology providers bring their banking and financial institutions clients to collaborate to build seamless digital journeys on the ONDC platform.

As ONDC continues to grow, the partnership between technology providers, financial institutions, and other stakeholders will be essential in ensuring that the benefits of digital commerce reach every corner of the country, paving the way for a more inclusive and equitable financial ecosystem.