I began this three-part series on 871(m) by quoting one of America’s most famed political characters and Founding Father, Benjamin Franklin. In order to round this series off in the same fashion, I’ll turn to another American political figure, this time: Abraham Lincoln. He was once quoted as saying “you cannot escape the responsibility of tomorrow by evading it today”, which I think quite accurately summarises the mantra that banks should be taking when it comes to 871(m), Transaction Tax processing and looking to the future.

So where do we stand currently with 871(m)? Banks must comply with the first part in the here and now and although the second part may still be under review, there’s absolutely no indication that the rule will be dropped in totality. I stand by what I said in the first blog – if banks are to wait until the full outcome of the review, they will only open themselves up to a plethora of problems later on. Banks do not want a repeat of five years ago, when they decided to implement tactical solutions for the French and Italian Transaction Taxes.

Of paramount importance for preparing for a post-871(m) world is that banks have software in place that can assist in facilitating a flexible ‘rules-based’ workflow solution which can easily adapt to changing legislation. From our extensive investigation of the intricacies of this, and other regulations which are on the increase, we found that due to the complexities of all, it makes little sense for firms to have multiple interfaces with the same derivatives and trading systems going to siloed tax solutions e.g. an FTT system in one place and an “871m machine” or system in another place.

It, therefore, makes much sense to feed it all into one solution and processing engine, rather than having a whole host of separate systems and trying to interface them all, which leads ultimately to more static, more cost and more fails (i.e. transactions). By taking a centralised or utility approach, banks are also in a good position to deal with even more potential incoming Transaction Taxes which is key in preparing for the future.

A resourcing and knowledge challenge

Alongside the need to assess which systems will be best placed or built to cope with 871(m), there are significant amounts of data that need to be pulled together, including dividends and trades across many different instrument types, potentially creating large integration projects for in-house teams. Place these needs against the backdrop of other current in-house IT initiatives that banks are aiming to achieve regulatory compliance with, and it becomes an even more complex resourcing and knowledge challenge.

Unfortunately, 871(m) is just one of many tax headaches facing banks, and more are certain to crop up further down the track. This is why taking a ‘future-proofing’ mentality is key here. Platforms and technology need to be fit to cope with other incoming regulations, so banks need to look at who can help them overcome these compliance headaches and who can demonstrate that they truly understand the needs and will provide “safety in numbers” when the regulator “comes knocking”.

871(m) won’t simply disappear by not thinking about it now. It’s the banks’ responsibility to prepare for the tax world of tomorrow, today.

By Daniel Carpenter, head of regulation atMeritsoft

Chris Rauen, Senior Manager, Solutions Marketing at SAP Ariba

If you have an electronic invoice system that just about meets the needs of the accounts team, but operates in complete isolation from the rest of the company, is that a system that provides much value?

It might do — if you’re doing business in the 1990s. Since then, a plethora of electronic invoicing systems have entered a crowded marketplace, all looking to streamline the complex way of processing invoices globally.

In today’s digital economy, new business value comes from linking invoice data to contracts, purchase orders, service entry sheets, and goods receipt for automated matching. Furthermore, automation of the invoice management process must extend beyond enterprise operations to include suppliers. Yet few platforms enable this. By treating accounts payable as a department, many e-invoice systems fall short of their potential.

So, how can linking electronic invoicing with a company’s other operational systems, and to suppliers, unlock this value? It turns out that an interconnected approach to invoice management in a digital age reduces costly errors, strengthens compliance, and facilitates collaboration both within the organisation and among trading partners.

A cloud-based network can assess trading partners against hundreds of criteria, including whether they can root out forced labour from their supply chain to how well they document the use of natural resources, and even giving work to minority suppliers. Of course, while software alone cannot ensure compliance with the ever-changing policies that continue to come into effect, it remains a powerful tool towards efforts in achieving it. Compliance, once a tedious task, now can be managed from a dashboard.

To reduce invoice errors effectively, a digital network must rely on intelligence — not just the human kind, but through smart invoicing rules that are essential to a business network. These rules effectively validate invoices before posting for payment to streamline processing, reduce operating costs, lower overpayment and fraud risk, and maximise opportunities for early payment discounts.

By enabling real-time collaboration between buyers and suppliers, digital networks not only bridge the information gap that can delay invoice processing, but they also reduce the complexity often associated with compliance. That includes effectively screening suppliers and monitoring business policies automatically before a transaction takes place.

However, perhaps the greatest advantage of digital networks is collaboration. Issuing an invoice, even when accurate and on-time, can sometimes be a one-way, asynchronous conversation. A buyer receives an agreed-upon product or service from a supplier, who at a later date sends out an invoice and, at an even later date, receives payment. This scenario has been the same for decades. But digital networks challenges that. The immediacy of network communications begs the question: Should electronic invoicing merely replicate the age-old process that postal mail once facilitated? Or shall it improve upon it?

We continue to see chief procurement officers choosing the latter. Through their day-to-day experience with digital networks, they have come to view invoice processing as just one part of the wider exchange of information among trading partners. An electronic invoice reflects a snapshot of the multi-party collaboration that networks enable, and — through intelligent business rules — alerts of potential errors or exceptions relating to the transaction. As we move forward in the digital age, and buyers and suppliers extend their relationship to include product design, innovation and product delivery, they are able to expand the scope of electronic invoicing to capture up-to-the-minute progress reports on the teamwork within and across organisations.

Ultimately, your electronic invoicing system shouldn’t focus only on accounts payable, it should give open visibility onto the rest of your operations and even who you do business with – so that mutual growth can be achieved and positive collaboration can flourish.

The author is Chris Rauen, Senior Manager, Solutions Marketing at SAP Ariba, the company behind the world’s largest business network, linking together buyers and suppliers from more than 3.4 million companies in 190 countries

Buzzwords such as ‘Artificial Intelligence’, ‘Machine Learning’, ‘Chatbots’ and ‘Robo-Advisors’ are rather ubiquitous among bankers and non-bankers alike. They are prominently echoed in boardrooms and earnings calls of large corporations, and increasingly feature in their quarterly reports. A few years ago, these ideas were merely discussed and not much was done to act on any of them. This could either be because of the lack of knowledge regarding the potential benefits these new technologies brought in, or because of the supposedly more important ‘strategic’ initiatives piled up on the desks of top management. This attitude has significantly changed over the past few years – one can notice a tectonic shift in the adoption of disruptive technologies for streamlining business processes, and in turn reducing costs and increasing efficiency. Large enterprises are implementing sophisticated solutions to internal processes, as well as to customer facing services, by using automation to replace repetitive, human tasks.

One such improvement in recent years has come in the form of Chatbots. The word ‘chatbot’ is a beautiful amalgamation of two of mankind’s most recent obsessions: messaging (chat) and robots (bots). Until recently, chatbots featured more in science fiction than in the real world. Few were able to fathom the explosive growth that was to occur. With the introduction of Siri, Alexa, and Google Assistant a few years ago, this bit of science fiction became a reality.

Chatbots are software programs that use real-time messaging as an interface. With extensive, and precise mapping of (potential) conversations, chatbots pose a serious threat to the age-old concept of a contact center. We now live in an instant gratification society, where waiting for an attendant at the opposite end has become a hindrance. In a world inhabited by digital natives, EVERYTHING IS INSTANT; from Instant Coffee & Noodles, to the more recent, Instant Customer Service. Chatbots are trying to address the latter, by providing real-time responses to customer queries. Be it rule-based or AI-driven, chatbots are slowly becoming the preferred form of communication for customers of all ages.

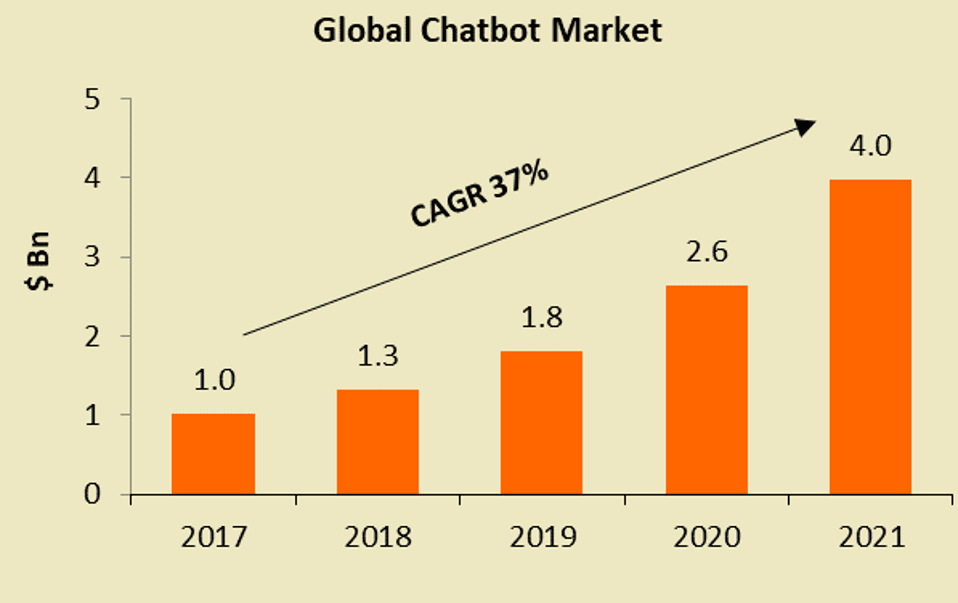

As a market valued at a little over $1 Bn in 2017 and predicted to reach $4 Bn by 2021, chatbots are set to grow at a CAGR of 37% over the coming 4-5 years. Looking at India for instance, in 2017, there were over 150 million users of messaging apps. This number is expected to grow at a CAGR of 17% over the next 3-4 years to 231 million users. With such rapid growth expected, companies are poised to ride the ‘chatbot’ bandwagon. This growth is driven by an increasing number of users relying on messaging apps, such as Facebook Messenger, Slack, and Telegram. In terms of cost reduction, chatbots will be responsible for annual savings of ~$8 Bn by 2022. And in terms of increased efficiency, a chatbot inquiry will save more than 4 minutes per call in comparison to traditional call centers. Is it surprising then, that enterprises are increasingly moving towards chatbots to reduce costs?

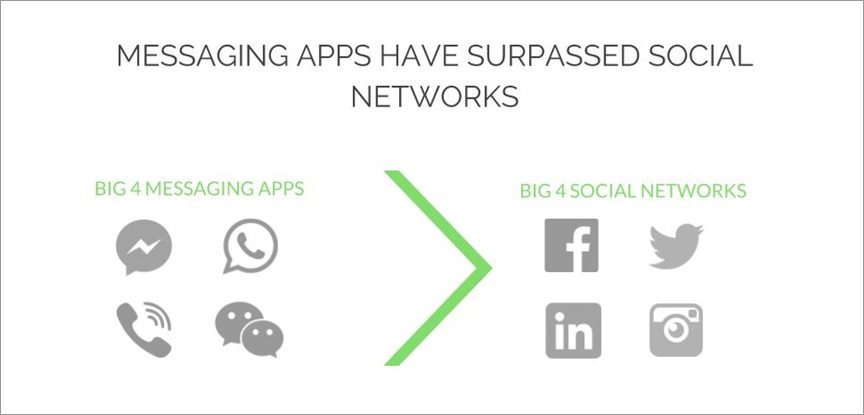

For any company, cost reduction and increased efficiency are in fact, imperative to its bottom line. What a chatbot, an automated chat interface, brings to the table is the ability to replace archaic contact centers, with a modern, instant service platform, at a fraction of the cost. A testament to the growth of messaging apps, and in turn to the rise of chatbots, is in its popularity; the top messaging apps garner a larger daily/monthly audience than the top social networks.

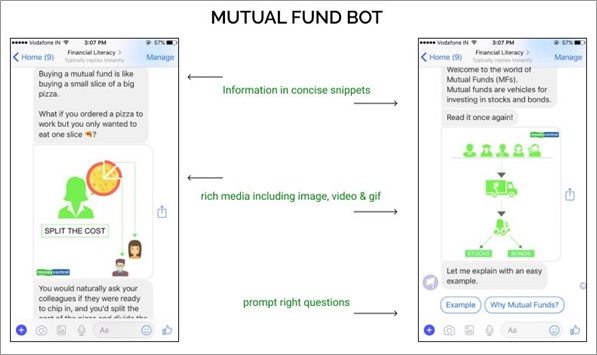

Translating this growth into tangible results for the financial services industry, is what many institutions are trying to unravel. Selling financial concepts is difficult, not because of the competition, but because of the prevalent status quo of doing nothing. There is a ton of information available, but this information is not designed to be digested by millennials, as well as by senior citizens. This is where Chatbots jump in! They can be positioned as utility tools to promote ‘Financial Literacy’, and disseminate information based on customers’ needs. For e.g., a Brokerage house can use chatbots to ‘educate’ new/existing users about the convoluted world of equity markets. Using an automated chat interface, complex financial terms and concepts can be simply explained, even to a novice. Typically, a chatbot determines the suitability of a product for a customer by assessing the financial health of his/her portfolio, along with the respective goals. The chatbot then recommends what products the customer should invest in, and what proportion of his/her wealth should be invested in different product types. The core objective is to empower the end user, who can then make informed monetary decisions after thorough assessment of the relevant products. The idea is to systematically break down complex financial content into conversational snippets within a chat interface. The content should be designed to enable the user to understand concepts and financial processes with ease, so as to bridge the gap in his/her understanding.

Source: Mpower.chatLet’s take Mutual Funds as an example. In India, Mutual Funds are becoming commonplace, given that they strike the right balance of being highly profitable, yet relatively safe. The share of MFs in the overall asset pie is increasing. There are numerous first-time investors looking to channel their moderate savings into high yield investments.

Although, the process of investing in Mutual Funds may seem straightforward, it is riddled with roadblocks (e.g., lack of financial know-how), some of which can easily (and rapidly) be countered with the help of chatbots. An effective chatbot can resolve certain customer queries within seconds, and if executed accurately, can put the customer at ease, thereby increasing his/her propensity to move ahead with that particular product or service.

On the banking side of things, large financial institutions such as Citi, Bank of America and Capital One have implemented their versions of chatbots, which customers can access through the respective mobile apps, Facebook Messenger, Twitter or regular text messages (SMS). At Citi and Capital One for example, customers can check their account balances, recent transactions, payment history, credit card bill summary, and avail many other non-financial services. Answering FAQs is one of the other key service areas where banks have excelled. All of these services collectively provide the user with real-time, easily accessible customer information. As a natural move forward, albeit on the slower side, banks are now implementing chatbots that allow customers to carry out financial transactions on their platforms; something that seemed generations away, doesn’t seem that far-fetched after all.

The need of the hour is communication, with its delivery through messaging applications dominating the social media & messaging landscape. These applications have far surpassed social media in terms of total users as well as total time spent. There are over 300 million people across India alone that have access to the Internet on their smartphones today, and India is embracing the Internet in a way we could not have imagined before. Keeping this development in mind, imagine a world where we use automated chatbots to not only breakdown financial concepts for seasoned smartphone users, but also help new internet users navigate through a plethora of financial information. The idea is to spread financial literacy, and create a more meaningful customer journey, from curiosity to execution. And chatbots make this accessible, by reaching customers via apps they already use – WhatsApp, Facebook Messenger, and Twitter – rather than making clients download additional apps.

The advent of chatbots (messengers, as well as voice recognition applications) has allowed companies to penetrate, through smartphones, the potential user base like never before. The primary use case for chatbots, in this day and age, is non-financial in nature. Most financial institutions allow customers to access only basic product information, and information regarding certain processes on their chatbots. However, with regulatory authorities taking a closer look at integrating such technologies into financial transactions, it won’t be too long until we can safely say “Alexa, please transfer $500 to Patrick this Thursday”, and rest easy.

By Abhijit Aroskar, Consultant, Cedar Management Consulting.

Data volumes are not just growing, they are exploding. Now measured in zettabytes – which could become yottabytes in the not too distant future – it’s not surprising they are causing more than a headache for today’s organisations. These vast pools of data are also putting traditional database architecture to the test.

Nowhere is this problem felt more acutely than in the banking industry, where the situation is exacerbated by a complex raft of issues. For example, many banks have had the same legacy systems in place for decades.

Often these are not fully-integrated with others in the organisation and, consequently, many applications still run in a siloed environment. In a recent study by analyst firm Enterprise Strategy Group (ESG), commissioned by InterSystems, 38% those polled reported that they had between 25 and 100 unique database instances, while another 20% had over 100. Although this was a general survey, not confined to the banking industry, it does give some idea of the scale of the problem.

So although many banks own these vast amounts of data, many of them are unable to do anything with it, especially analyse it in real-time. Which means that often they just don’t have the capability to provide the open banking demanded by new regulations such as PSD2.

Banks have been addressing new regulations in a piecemeal fashion for too long and this approach is now catching up with them. With each new ruling they have put a new siloed application in place to meet its specific needs and no more – but there’s a limit to how long this can continue. Today’s regulations are demanding an end to data siloes with integration enterprise-wide and the ability to analyse data in real-time.

These are broad-brush requirements. At a more granular level, banks must think through the step-by-step processes needed to meet compliance. Typically, they will need to bring information in from multiple applications, run reporting on this data on a real-time basis and generate that in a format that meets the regulator’s precise requirements.

As a result, banks must seek out a data platform that can ingest data from real-time activity, transactional activity and from document databases. From here, the platform needs to take on data of different types, from different environments and of different ages to normalise it and make sense of it. The platform they select must be about to reach out to disparate databases and silos, bring the information back and then make sense of it in real-time.

This platform must also have the agility to separate out the data they need from the data they don’t need to access. It is also the case that, as businesses migrate systems and applications to the cloud, they are beginning to use software to ‘containerise’ their applications and modules. Once these containers have been set up in the cloud, they are then reusable by other applications.

It is crucial that a data platform enables data to be interrogated even if it is in large data sets and stored in different silos. This capability is important to enable the bank to comply with regulatory requirements such as answering unplanned, ad hoc questions from the industry regulators, for example.

The advantage of working this way is that it can take the bank far beyond compliance. It will now have a secure, panoramic view of disparate data which can be used for distributed big data processing, predictive and real-time analytics and machine learning. Real-time and batch data can be analysed simultaneously at scale allowing developers to embed analytic processing into business processes and transactional applications, enabling programmatic decisions based on real-time analysis.

So although many banks and other financial services organisations may feel they are being swallowed up by data, the need for compliance will ensure this doesn’t happen. The more they are storing on legacy systems, the more they are going to need an updated data platform. If they think carefully about selecting the right one, the move could result in improvements across data management, interoperability, transaction processing and analytics, as well as the means to address today’s and tomorrow’s regulatory demands.

By Jeff Fried, Director, Product Management – Data Platforms, InterSystems

Karen Wheeler, Vice President and Country Manager, Affinion

It would come as no surprise if internet retailer Amazon announced it was taking over the world tomorrow. There seems to be very little that it can’t offer customers, whether it’s conquering Christmas lists, watching boxsets through Prime or managing life admin through the intelligent personal assistant Alexa, almost everyone uses one or more Amazon service on a regular basis.

One common denominator that defines Amazon’s success across all of its platforms is customer experience – providing simple, convenient and engaging solutions that go that extra mile to ‘wow’ customers and retain their loyalty.

Banks, however traditional or modern, can take a leaf out of Amazon’s book when it comes to engaging with customers and harnessing innovation to continuously improve their offering.

Here are five important lessons banks can learn from Amazon.

The customer always comes first

Listening to what the customer wants has been the driving force behind many of Amazon’s products and developments. McKinsey’s CEO guide to customer experience advises that the strategy “begins with considering the customer – not the organisation – at the centre of the exercise”.

This can often be quite a challenging ethos for the banking sector to buy into, particularly for the more traditional bricks-and-mortar companies where the focus is often on the results of a new initiative, rather than the journey the company must take its customers on to get there.

It’s a case of convincing senior management that the initiative is a risk worth taking and just requires some patience. Amazon originally launched Prime as an experiment to gauge customers’ reactions of ‘Super Saver Shipping’ and it was predicted to flop. Nowadays it’s one of the world’s most popular membership programmes, generating $3.2bn (£2.3bn) in revenue in 2017, up 47 per cent from 2016.

Create trends rather than follow them

To stay ahead of the curve amidst the flurry of digital fintech start-ups, banks need to come up with their own innovative customer experience solutions, rather than allow newcomers to do so first and then follow suit.

From the customer’s perspective, a proactive approach will always go down better than a reactive one. Amazon CEO Jeff Bezos has previously spoken about tech companies obsessing over their competitors and waiting for them launch something new so that they can ‘one-up’ it. He once wrote: “Many companies describe themselves as customer-focused, but few walk the walk. Most big technology companies are competitor focused. They see what others are doing, and then work to fast follow.”

What sets Amazon apart is listening to what the customer wants and prioritising them over competitors.

A great example in the banking sector is mobile-only bank Starling, which recently announced partnerships with several financial service providers that customers can quickly access via its in-app ‘Marketplace’. The first to become available is PensionBee, a digital pension provider that aims to consolidate pension pots into one. Others, including a digital mortgage broker and a digital wealth management service, are soon to follow.

Ultimately, Starling listened to and understood its digitally-minded customer base who, like most people, see shopping around for financial providers complicated and admin-heavy. One central app where you can seamlessly select a trusted digital partner would no doubt go down as good customer experience.

Use customer data to form any new idea

It’s no secret that Amazon is one of the leaders that has paved the way for analytics. It’s through the company recognising the need for them which has led to customers becoming accustomed to personalisation and expecting it as soon as they have had their first interaction with a business.

Banks are no exception to this and, while it may seem like a scary commitment to more traditional firms, it doesn’t have to be complicated. A classic, simple example is Amazon storing customers’ shopping habits and sending them prompts for new products similar or related to those they have purchased in the past.

In the financial world, digital bank Monzo is leading the charge by monitoring customers’ spending habits to offer them financial advice to help them save money and budget responsibly. For example, its data once showed that 30,000 of its customers were using their debit cards to pay for transport in London – so Monzo can advise them they could save money if they invested in a year-long travel card, for instance.

There are endless things banks can do using customer data to provide the customer with an experience unique to them, rather than continuing to make them feel like just another cog in the wheel. At Affinion we believe in ‘hyper-personalisation’, in that these days it’s no longer good enough to just know a customer’s history of transactions with a company and when their birthday is.

Customers are getting more tech-savvy by the day and are expecting real-time responses with a deep insight into their interactional behaviour – they won’t remain engaged if follow up contact is irrelevant and untargeted. Customer engagement has moved on from companies communicating to the masses, it’s about creating tailored, intuitive relationships with them on an individual basis.

Widen the offering beyond traditional banking

The way we live as a society is forever changing and, as we get busier and busier, any small gesture to make life that little bit easier goes a long way. The consolidation of services such as banking, insurance, mobile phone networks, utilities and shopping is a great way to ensure customers remain loyal to a brand as it will – if done right – add value and reduce hassle to their lives.

As an expert at disrupting industries, Amazon has taken note of this growing need for convenience over the years and has expanded its offering for customers, allowing them to carry out multiple day-to-day tasks with one account. In the last few months alone, Amazon has hinted that it may acquire a bank to break into the financial industry and potentially start its own healthcare company.

Regardless of size, banks should always be looking for new areas they could tap into to broaden their offering and show customers that their needs are at front of mind.

Engage with customers through goodwill

A rising factor in the way that customers align themselves to a brand is its stance on ethical issues and its contributions back into society. It’s a shift that seems to be most prominent with Generation Y, as the Chartered Institute of Marketing found that 81 per cent of millennials expect companies to make a public commitment to good corporate citizenship and nine in 10 would switch brands to one associated with a good cause.

Amazon has gone that one step further, with its AmazonSmile initiative that allows the customer to choose a charitable organisation that it will donate 0.5 per cent of eligible purchases to. Not only does this show Amazon’s commitment to charitable causes, it gives the customer control of where their money ends up.

This is an easy win for the banking sector, given that one of its sole purposes is to look after money and move it around. For firms that target younger generations in particular, looking at ways to involve customers in charitable donations in a fun, transparent and seamless way is a no-brainer for increasing loyalty and advocacy.

It’s time banks took customer engagement even more seriously

For many people, personal finance is perceived as a chore and often quite complicated. Improving the customer experience and building in programmes to engage them can help greatly with this and banks need to adopt the ‘customer first’ ethos that Amazon showcases so effortlessly. With new fintech disruptors creeping into view, keeping customers loyal and engaged has never been so important.

By Karen Wheeler, Vice President and Country Manager UK, Affinion

Georges Berzgal, vice president EMEA, global ecommerce, Pitney Bowes

For the first time ever, eWallets such as PayPal and Alipay are outpacing credit cards as a method of payment for cross-border online shopping. The emerging trend, identified by Pitney Bowes in its 2017 Global Ecommerce Study1, raises concerns for online retailers accepting only credit cards as a payment method. With 70% of consumers now shopping online outside their own country, businesses must respond to consumers’ changing payment choices or risk losing customers at the checkout.

Fully 41% of global respondents surveyed use eWallets as their preferred method of payment, more popular than using credit and debit cards, bank transfers or mobile wallets. This varies from country to country, with the figure as high as 64% for shoppers in Australia and 61% for shoppers in Germany. Year-on-year growth is highest for Mexico, which has seen a rapid increase of 37% in the number of cross-border shoppers using eWallets since 2016, and a decline in the number of credit cards as a preferred payment option. This popularity of eWallets is reflected in figures collated by Statista, which identified that in the third quarter of 2017, over 218 million PayPal accounts were active worldwide2, a figure which has increased every quarter since 2001.

Marketplaces driving eWallet take-up

Consumers are increasingly using marketplaces – such as eBay and Etsy – for their online shopping. 62% of online cross-border shopping is spent on marketplaces as opposed to 38% on retailers’ own websites, according to the Pitney Bowes study. Marketplaces widely accept eWallets as a method of payment, so the trends may well be interconnected: consumers become more used to the convenience, and it’s easier to check out when mobile shopping, so it could be that marketplaces are driving up the use of eWallets.

However, there are some variations in eWallet usage between countries. Shoppers in Germany primarily use eWallets, by far the most popular method of payment for cross-border shopping: 61% prefer this method, followed by 26% credit cards and 10% mobile wallets. India is the only country which equally uses credit cards, eWallets, and debit cards or bank transfers. Yet eWallet hasn’t gained traction so far in Japan, Hong Kong, and South Korea, where credit cards are still the main payment option for cross-border purchases.

Buyer protection

The study also revealed that 21% of respondents are concerned that personal information could be compromised. In the US, this figure rises to 30%. eWallets bring with them strong levels of buyer protection, and buyers are aware of this: PayPal, for example, monitors transactions 24 hours a day, seven days a week, and transactions are encrypted, too. Buyers can even be reimbursed for damaged or missing items. The more security-conscious buyers become, the more attracted they will be to those payment methods which provide them with better protection. Credit cards, under the Consumer Credit Act, must provide protection for purchases over £100 and below £30,000, but many online transactions fall below that threshold. A debit card does not carry the same reimbursement protection, although most major banks will flag unusual transactions and contact their customers accordingly. With this in mind, it becomes clear why eWallets are increasing in popularity.

Mobile wallets still in early stages of adoption

The study also researched the take-up of mobile wallets such as ApplePay. Just 4% of consumers, on average, said this was their preferred payment method when shopping online cross-border. The study shows that the payment method is still in its infancy in the majority of countries surveyed. China and South Korea have the highest levels of adoption, at 10% and 7% respectively, and the US follows closely behind at 6%. Across Europe especially, the take-up rate is low, and although the UK’s adoption rate is consistent with the global average of 4%, France’s usage has dropped since last year.

This could be because consumers are using mobile wallets for in-store, physical purchases of lower value, and prefer alternative methods of payment for shopping online, but more widespread usage in physical transactions is likely to influence usage for digital transactions – if you’re using it in Costa, for example, you’re more likely to turn to it if offered it on a retailer’s website. It could also be that further education is required before retailers include ApplePay as a payment method on their ecommerce sites.

Payment power

With average cross-border order values (AOV) 17% higher than domestic AOV, it comes as no surprise that 93% of retailers plan to offer cross-border shopping by the end of 2018. However, as retailers extend their businesses overseas, they must take time to identify the preferred payment options for shoppers in each region and to look at growth in payment methods. It isn’t just a case of ‘We’re expanding to China, we should offer Alipay.”

For some regions, payment methods are the result of cultural behaviours: some countries have an aversion to building debt, and fees may discourage merchants’ acceptance of credit cards, which makes their usage a less common practice.

Understanding these preferences is crucial. One in five shoppers are put off if their preferred payment option isn’t available – that’s 20% of potential business. With $4 trillion worth of goods left abandoned at the online checkout, retailers can’t afford not to address this3.

In the study, 37% of consumers surveyed said they would be more willing to buy cross-border if they were given payment options they prefer. This figure rose to 49% for India, 48% for Germany and 47% for China. It was cited as higher in importance than offering discounts and sales; than offering an easy returns process; and was even preferred to offering native language on a website.

Ecommerce companies must track emerging payment trends

Businesses must look at the emerging payment trends and currency preference for each country, as well as those methods which are in decline. Retailers are already exploring accepting Bitcoin and other cryptocurrencies, for example. Subway accepts Bitcoin, and Microsoft and X-Box do so for some transactions. Some retailers are hesitating, however, due to its fluctuations, with only three out of the top 500 online merchants4 offering it but again, this differs from country-to-country: China and Japan are two of the countries with highest Bitcoin take-up, according to a report in Business Insider5.

Historically, it’s fair to say that technology disruption in payment methods and preferences have been on the slow side. Now, digital transformation is accelerating the pace of change. Businesses need to understand the differences in consumer behaviour and preferences country by country and structure their business to respond to this change.

By Georges Berzgal, vice president EMEA, global ecommerce, Pitney Bowes

In the third of this three-part article series on the effect of the 871(m), Daniel Carpenter, head of regulation at Meritsofttakes a look at some of the unintended consequences the finance industry may face once the ruling is fully enforced.

Speaking at the Vantage Melbourne rise of AI and automation conference last quarter, Telstra’s head of innovation, Stephen Elop, said that the “path to disruption is paved by unintended consequences.” This sound bite by no means only applies to the world of telecoms, it also relates to financial firms getting their houses in order for the impending 871(m) tax regulations.

Although it’s hard to imagine this looming change to the tax system having quite the same effect as the influence of AI, there will still be unintended consequences. The primary issue is whether 871(m) could reduce market participants interest in U.S equity derivatives products covered by the U.S Internal Revenue Service’s (IRS) rules.

It’s certainly a possibility, as confirmed by a senior tax specialist and Foreign Account Tax Compliance Act (FATCA) practitioner at an ‘871(m) lessons learnt in 2017 and what is around the corner for 2018’ seminar towards the end of last year. With the second part of 871(m) legislation, which is currently being finalised, scheduled to come into force in January 2019, 871(m) legislation is unlikely to be revoked.

But it isn’t as easy as simply deciding not to trade certain derivatives products covered by the 871(m) rules. One head of securities tax at a leading accountancy firm explained that they have found that clients have been unable to switch off U.S securities, in the context of securities lending, even if they wanted to. While firms might try to say that they don’t offer any service in U.S securities, they ultimately will because they’ll receive it in the form of collateral, for example.

Essentially, it’s near impossible to just tail-off U.S products, like an index or a basket of securities where an American company name pops up. While some of our attendees at the event explained how a number of their clients had made a conscious decision to disavow any kind of U.S strategy, they still end up with them. Although you can limit their exposure, you simply can’t exclude them altogether.

One expert revealed that his firm had also had discussions about whether, if you were on the ‘Long’ side, you could just use a U.S broker so that you would never have to withhold (i.e. through a ‘W9 form). However, he rightly pointed out that MiFID II and best execution requirements mean that it couldn’t be done either, aptly stating that “all of the sensible things one might think you could do just don’t work”.

While we should not, by any stretch of the imagination, be expecting the same sort of significant changes AI will bring to the telco industry, when it comes to 871(m), and many other new transaction taxes, we should definitely be considering them in whatever form they materialise, and addressing the potential inadvertent outcomes now is of the utmost importance.

Payments have come a long way since the days of waiting for a check to clear in seven days, paying for goods is now possible from anywhere at any time, on any device. What’s more, these purchases are no longer exclusively domestic. From the smallest micro-merchant to the largest corporate, trade and therefore transactions are now truly international.

However, the timeliness, complexity and opacity of international payments is still a very real challenge. Even in light of disruptive and far-reaching technological innovation, this basic and fundamental problem remains unfulfilled. Which begs the question – Why isn’t there a standardised approach for global, cross-border payments compatible with today’s immediate, digital economy?

New age of payments

SWIFT is the current de-facto network for international payments and has the benefit of wide reach through being bank-owned and ingrained in the global financial system. Although it is the most widely accepted cross-border payments infrastructure, it is based on the 600-year-old correspondent banking system and therefore slow and filled with inefficiencies.

SWIFT’s nascent rival, Ripple, is based on blockchain and crypto technology and can provide speed and certainty that are effectively unmatched in today’s market. Although it has attracted major financial institutions to pilot its platform, it does not yet have the scale or reach of global infrastructures and is still effectively utilizing a correspondent banking network.

The competition is clearly having an effect, as SWIFT recently completed a “proof of concept” test of blockchain technology finding, unsurprisingly, that blockchain technology needs to make more progress before it can handle the billions of dollars of daily cross-border payments between the world’s banks.

Is Instant the answer?

There’s a new player throwing its hat into the ring: the Cooperative model of Instant Credit Transfers.

43 countries are now using Instant Payments infrastructure domestically, including major economies such as Australia and the US. This begs the question as to whether primarily domestic networks can interoperate to create an international one.

SCT Inst partially answers that question by creating a pan-European, Instant Payments service linking those domestic instant payments schemes. SCT Inst enables transfers of up to €15,000 within 10 seconds, 24/7, to any of 34 SEPA territories – across multiple CSMs but still in the same currency. But is this enough to work on the global stage?

Inter-governmental considerations aside, from a technical perspective the answer is yes – those hurdles were overcome when we learned to make international phone calls reliably. The topic of FX conversions [the only cross-border consideration not addressed in SCT Inst] isn’t really a barrier either – just an item on the plan to work through.

And the payoff is significant. for the vast majority of transactions because payments are processed immediately, whether successfully or otherwise, there is no inefficiency in the form of delays or payments. Since more banks will participate directly, rather than through a correspondent, the cost will likely come down significantly, with fees trending towards domestic pricing and FX rates towards interbank with small margin on top. The transparency will also be improved – senders will be fully advised of any delays to a transaction.

That said, sending money to “difficult” jurisdictions through Instant Payments could be one of the main sticking points in implementing a truly global system. Even if these geographies have or develop schemes in the future, current operators will be reluctant to connect to it, or banks will make sending payments to these territories prohibitively difficult. It is in those jurisdictions we see most cost and delay, and that is unlikely to change. Clearly, just having the technical capability is not enough; it must be supplemented by regulatory framework and woven into laws and industry practices.

Cross-border instant Payments may well be the catalyst for a new wave of innovative corporate banking, payments and cash management services. And since it has the benefit of starting from the already established domestic base, it may get to practical global ubiquity much faster than any of the competing approaches. It is the one to watch for in 2020.

By Gene Neyer, Chief Strategy Officer, Icon Solutions

While the benefits of fintech are being seen at increasing scale for consumers in the US, Europe and China, adoption among corporates is less emphatic. A recent paper from Wharton Business School highlights what many see as an ongoing challenge – the struggle between existing bank partners and new, challenger fintechs for that vital role with businesses, as they look to transact and manage cash.

Unfortunately, the competing pressures on corporate treasury are far more complex than this argument allows. We need only look to geopolitical factors that have had a knock-on effect on businesses, banks and treasury in recent (and not so recent) years. At this month’s EuroFinance conference, Strategic International Treasury, US tax reform is high on the agenda as businesses of all industries grapple with its implications. There certainly are opportunities following the legislation to adjust and re-think treasury activity, but there is no single approach, with it affecting different sectors and business models in very different ways.

Does this environment present an opportunity for investment in fintech from corporate treasurers? Certainly, but it’s equally useful to look at bank partners and ask – are they ready too? Myriad regulatory developments since the financial crisis mean that banks are potentially only now really ready to look at opportunities for game-changing, strategic technology that fintech provides. So where do the opportunities lie and how can we get there?

From siloes to an enterprise-wide perspective

For treasurers, a key challenge when coming to grips with the opportunities from fintech is attempting to understand the tangible benefits technology will deliver to their business as a whole. Organizational siloes prevent individuals from seeing how improved processes in one part of a business could either be beneficial or a burden in another. That enterprise-wide perspective is a crucial first step, before launching into a deep dive of whether DLT can benefit risk management in treasury operations.

That said, fintech needs to meet treasury in the middle by understanding the cultural differences between the two. Inertia may affect people in businesses because of the culture and habit around existing technology and incumbent infrastructures. If fintech aims to disrupt treasury then it needs to address how to solve existing problems and find ways of helping business in transformation. Just presenting smart new tech is not enough.

Business transformation has steadily evolved as a discipline to help overcome this very issue. For example, in the M&A process there is now an acceptance that merging two companies isn’t as simple as rationalizing costs, ditching an inefficient system and migrating data. Without understanding the people who will be adopting the technology, from CFOs and CTOs to accountants and cash managers, you aren’t laying the foundations for success.

Mass customisation: an achievable goal?

With the right mind-set, businesses can look to leverage the benefits from solutions that are steadily being developed by central and transaction banks, and fintechs. The speed and efficiency from AI and predictive capabilities, the effectiveness of work being done on emerging platforms and the learnings from pilot projects such as Hyperledger will all have lasting impact on treasury and related operations.

The most important thing to consider is how the specific use cases for each technology being developed can be made available at scale. Mass customisation is the missing piece in the growth of the technologies discussed above. There needs to be a shift away from a “one-size-fits-all” approach, to really reflect the pressing needs of individual treasury functions. Each treasury organization is part of a unique business with its own set of problems, so understanding this is the revolutionary change that businesses need to see in the solutions being offered by fintech and the banks.

About the author:

Robert J. Novaria has more than 30 years of corporate experience in the roles of treasurer, credit director, finance manager and controller at BP America and Amoco Corporation. Currently, he is a partner with the Treasury Alliance Group, leveraging his corporate experience in client engagements dealing with global treasury challenges, including risk and crisis management; cash management and cash flow forecasting; working capital management; shared service operations and general management. He also serves as a chairperson, moderator and speaker at treasury conferences worldwide.

For more information about EuroFinance: Strategic International Treasury and to book: www.eurofinance.com/miami

If there’s one positive thing about social media, it’s that it’s keeping everyone on their toes – especially service providers. Woe to the retailer, airline, bank, etc. that can’t keep its operations running so that they are available when and how users want them, 24/7, regardless of volume, transaction level, network congestion, or any other factor.

And the users are often merciless; just ask the folks in the IT department at banks like Natwest, Lloyds Bank, HSBC, Nationwide UK, or any of the other banks that experienced temporary service outages in December alone. Angry customers who couldn’t access their accounts, move their money, pay bills, or otherwise access banking services angrily vented their frustrations, using language that would make even sailors, in an ongoing barrage of rants against the institutions.

Ask any IT person whose managers are breathing down his or her neck for answers: It’s not an experience one would want to repeat. In fact, IT personnel likely resent being the ones left holding the bag when there is an outage; they may have recommended more advanced monitoring systems that management baulked at paying for, for example. They’re forced to make do with what they have – and what they have may not be up to the task at hand, ensuring service stability and presence during times of network stress, due to extra volume, network congestion, etc.

On the other hand, you can’t blame management for baulking at investing in the latest and greatest system that might solve outage issues, as opposed to systems that definitely will solve them. Vendors wax eloquently about how their solution is the solution to, for example, cybersecurity issues, but despite the money, companies throw at these solutions, hacking is as bad as ever. You can’t blame the C-suite folks from being sceptical when it comes to outage solutions, as well.

While IT departments might dither on cybersecurity solutions, the answer to their outage issues is already at hand – in their often overlooked but always important log files. These files provide a wealth of information about everything that goes on in an organization. Data from infrastructure, applications, security and IoT areas can provide insight into CRM, marketing, ERP and other initiatives for the business – as well as provide insights into why outages occur, and what to do about them.

But parsing through log files searching for actionable insights is a difficult job – too difficult for human beings. What’s needed is a machine learning, artificial intelligence-powered log analysis system – a system that enables its users to parse through unstructured data in order to develop actionable insights. Such systems allow users to define what they are looking for with a data structure, and feature an analytics system smart, fast, and robust enough to parse through thousands, if not millions of files and data streams.

It makes sense. Just think about the installation of a new piece of network software: How many DLL’s get written, how many dependencies are created, how many config files are adjusted? Too many to count, that’s for sure – and go figure out where all those changes were made. Yet one small “adjustment” in a config file could be enough to halt network traffic for hours. With AI-based log file analysis, however, it would be possible to prevent such outages; as soon as an unwelcome change is made, the system could alert IT managers and provide them with the exact information they need to resolve the issue.

And that AI-powered system could be used to analyze log files for many other purposes – providing organizations with insights about customer behaviour, expenses, better ways to do marketing – the list is endless. What’s needed is not a “new” system that will promise to solve a problem, like outages – but one like AI-powered log analysis, that will unlock the data companies already have.