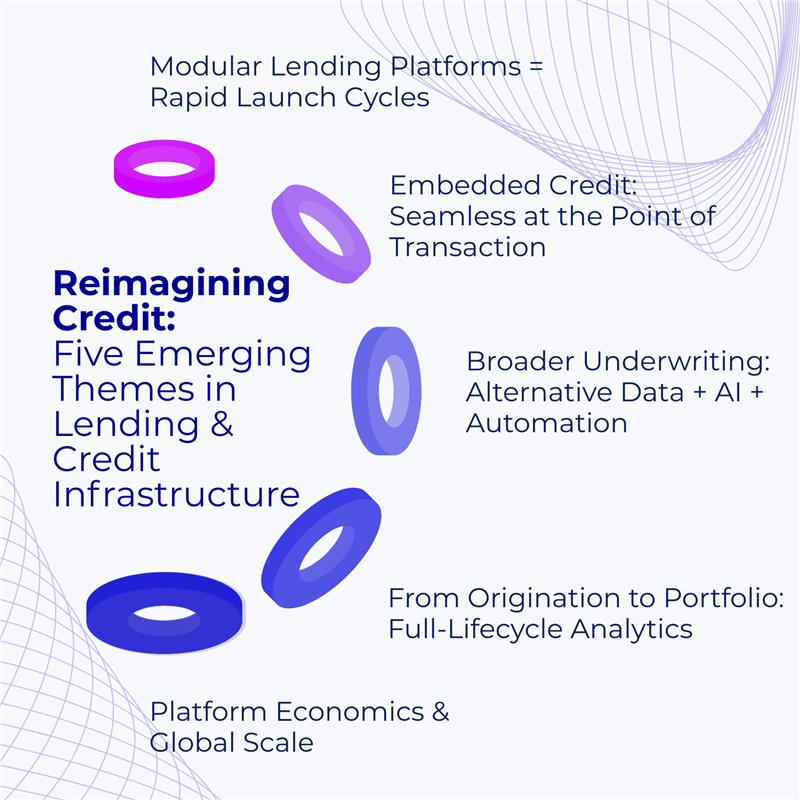

Reimagining Credit: Five Emerging Themes in Lending & Credit Infrastructure

November 24, 2025

Within our Cedar-IBSi FinTech Labs cohort of over 60 global FinTechs, we recently reviewed the range of solutions being built and deployed by our current members. One theme stood out above all: Lending & Credit Infrastructure. Nearly one in four Lab Members today focus on transforming how credit is originated, underwritten, distributed, and managed.

This isn’t just a product trend. It signals a deep shift in how financial institutions think about credit; from traditional, paper-heavy systems to modern, modular, and intelligent infrastructures. In this blog, we examine the current trends across the industry and their implications for banks as they navigate the future of credit.

- Modular Lending Platforms = Rapid Launch Cycles

Launching a new credit product once required months of development. Today, platforms like WonderLend Hubs are delivering no-code, micro-modular loan origination systems in a cloud-native, pay-as-you-scale model. Their platform has already processed over ₹8,500 crore in loans and ₹6,500 crore in incentive payouts (source: PR Newswire, 2025).

Similarly, SysArc Infomatix’s LENDperfect and CONNECTperfect solutions combine loan origination with more than 200 API integrations, connecting credit workflows to existing bank systems.

Why this matters: Flexibility is replacing rigidity. Banks and NBFCs can now roll out new credit products in weeks instead of quarters, with business teams, not just IT, managing the change.

- Embedded Credit: Seamless at the Point of Transaction

Credit is becoming an invisible part of business transactions. Lab member TransBnk merges transaction banking with lending flows, embedding working-capital finance and supply-chain credit directly into payment journeys. The company now processes over 110 million monthly transactions through more than 1,500 APIs, recently securing a US $25 million Series B to expand across Asia and the Middle East (source: Economic Times, 2025).

Why this matters: When lending is embedded into payment flows, businesses can access instant, contextual finance without friction a win for both customer experience and operational efficiency.

- Broader Underwriting: Alternative Data + AI + Automation

Legacy underwriting depends on static credit histories and manual document reviews. But that’s changing. WonderLend Hubs utilises a Socio-Economic Profiler, powered by location intelligence and behavioural data, to assess thin-file borrowers. Meanwhile, Cogniquest AI employs intelligent document processing to extract and analyse complex financial data in real-time.

Why this matters: AI-driven, alternative-data models make credit more inclusive and far more efficient, improving decision accuracy while expanding access to new customer segments.

- From Origination to Portfolio: Full-Lifecycle Analytics

True innovation in lending now extends beyond origination. Surya Financial Technologies delivers a suite of balance-sheet and risk-analytics tools, including Balance Sheet Navigator and Risk Navigator, used by banks in over 20 countries. These help institutions model risk, return, and capital dynamically, rather than retrospectively.

Why this matters: Lending infrastructure today isn’t just about faster onboarding, but about smarter management. Institutions that link origination and portfolio analytics gain a complete, data-driven view of performance and capital impact.

- Platform Economics & Global Scale

As the cloud reshapes banking technology, platform economics are redefining credit.

WonderLend Hubs operates on a subscription model that grows with its clients, while TransBnk’s international expansion shows how Lending Infrastructure-as-a-Service can scale rapidly across markets.

Why this matters: The shift from license-based systems to flexible, API-driven platforms is making enterprise-grade lending technology accessible to smaller lenders, driving competition, innovation, and global reach.

The Road Ahead

The lending industry is entering a phase where speed, configurability, and data intelligence have now become expectations. This means that Banks and NBFCs must think beyond digital channels to the architecture of credit itself: modular platforms, embedded financing, and lifecycle analytics will define the next decade of growth.

At Cedar-IBSi FinTech Labs, we’re proud to collaborate with the innovators building this future, transforming how credit moves through modern financial systems.